Press release – Tuesday 7 November 2017

Property Industry Alliance (PIA) Debt Working Group

UK property industry launches quarterly metric to warn lenders and regulators when price rises should signal lending curbs

- By understanding how overvalued property is relative to trend, banks and regulators can act to cut exposures

- Aim is to cut lending risks at market peak by providing early warning system. Current values 10pc above norm

- Adoption of metric by lenders and regulator will reduce risk to the UK financial system, say experts

Property chiefs have launched a new metric to sound an early warning for lenders and regulators when commercial real estate (CRE) values lurch too far above long-term norms.

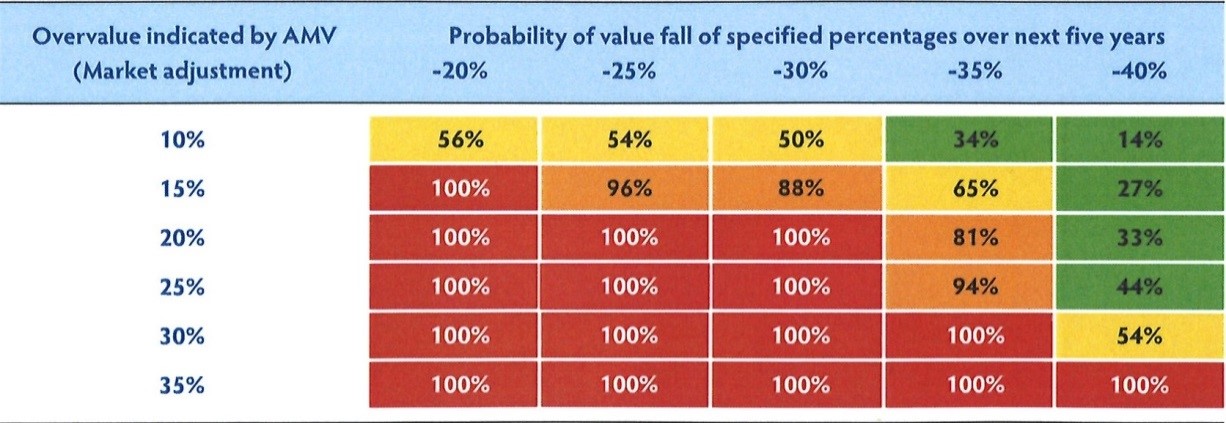

The adjusted market value (AMV) metric – one of three that was proposed – is effectively a percentage determination of how overvalued UK commercial property is. It has looked back over previous cycles, crunching data to work out how far values could go before a market crash becomes almost inevitable.

The move follows a series of research papers and is designed to allow regulators to rein in lending when the market gets too frothy – while helping banks better understand the risks they take at various points in the property cycle.

Based on the MSCI IPD All Property index for Q3, it shows CRE values are 10 percent above long-term average, once inflation is stripped out. It gives a 50 percent risk of prices falling by 30 percent within the next five years – rising to 100 percent if values hit 20 percent above average.

In the past, every time values have exceeded 20 percent above average, prices have crashed by at least 30 percent in real terms, research shows [see notes].

However, experts have emphasised that current lending levels are far more conservative than in the period leading up to the last crash.

According to De Montfort University (DMU), which surveys UK property lending each year, average loan-to-value ratios today are around 60 percent compared to around 75% in 2006/7

By adopting AMV, the property industry hopes that the Bank of England can pull regulatory levers to cut lending as a proportion of market value when those values rise avoiding a repeat of 2007.

Rupert Clarke, chair of the PIA debt group and managing partner at Lipton Rogers, said:

“Our ambition is that all lenders – banks, funds and debt funds – hard-wire this methodology into their risk metrics, become more cautious when it starts to hit amber and take decisive action when it moves into red. At the moment the vast majority of lenders have no clear action plans to prevent themselves from being sucked in the CRE lending “black hole”, lending too much against overvalued properties at the end of the CRE cycle.”

Peter Cosmetatos, chief executive of CREFC Europe, which represents property lenders, said:

“This is about giving regulators and banks a relatively scientific warning system to prevent lenders overextending themselves in a boom, suffering losses that prevent them from lending after a crash when the economy most needs credit. Adjusted Market Value isn’t a panacea – it needs to be used alongside other metrics, not least lending data – but its regular publication is a step change in promoting better property lending risk management.”

Rupert Clarke added: “The reasons we need this metric are that lenders and regulators consistently fail to recognise the risks at the end of the cycle, allowing their loan activity to spiral as property becomes increasingly overvalued, resulting in huge losses and the risk of financial meltdown.”

Charles Cardozo, director at Radley & Associates, said:

“This is the start, not end of the journey, as further technical work will need to be conducted on the methodologies to analyse and fine-tune the models. Rather than seek to alter the way market values are determined, what we’ve attempted to is offer a solid basis to supplement the information available to lenders and the regulator, with a metric specifically intended to inform risk management and regulatory capital requirements.”

Vicious circle as price increases spur lending

Lending activity usually rapidly increases towards the end of a property cycle. CRE values sore, and as lending grows too, this amplifies risk. Because lenders are incentivized to lend money, the majority of losses are linked to end of cycle loans.

DMU’s research showed that after lending a record breaking £82bn in 2006, 89% of CRE lenders planned to increase their new lending activity in 2007. All last cycle CMBS write-offs related to issues between 2005-7, according to Fitch.

Led by the Property Industry Alliance (PIA), a collection of trade bodies representing investors, developers, surveyors and lenders,, the risk analytics consultancy, Radley & Associates, has developed AMV to show the percentage by which prices are above or below their long-term historical trend level based on all types of property and establish the probabilities of such overvaluations leading to major falls in values

The majority of the work has focussed on establishing the vulnerability of the market as a whole using MSCI IPD’s headline benchmark. At present, there is no mechanism to establish a similar clear link between overvaluation of any particular sub-sector, such as retail or City offices, and an impending crash due to insufficient data.

Since the 2007 financial crisis, central banks and regulators have employed mechanisms such as slotting which demand increased levels of regulatory capital to be set aside by lenders. While it is now seen to have been relatively effective at constraining excessive CRE lending, slotting is not applied consistently and there is certainly opportunity for growing competitive pressures to start loosening those constraints in future.

Years of research

The UK property sector has spent years analysing how it could avoid another massive market failure. In 2014, it published a milestone report A Vision for Real Estate Finance in the UK which set out how lenders and regulators could better understand and manage the risks that occur during every property cycle.

The Vision report identified a number of measures to usher in a “more stable, efficient, diverse, and transparent market with greater liquidity, lower risk and better pricing”. And in June 2017 a follow-up report exploring three alternative long-term value methodologies was published by a PIA debt working group, led by former Hermes Investment Management chief executive Rupert Clarke, a former BPF president who is now managing partner at Lipton Rogers, a development business formed with Sir Stuart Lipton and Peter Rogers.

Objectives of AMV

- Dampen credit growth during a boom, reducing the potential for regulated lending to feed a CRE bubble by breaking feedback loops between valuations and lending

- Avoid discouraging relatively low-risk CRE lending after a crash, when investment in the sector is most needed.

- Establish a through-the-cycle measure against which point-in-time collateral values can be compared on a loan-by-loan, loan-book, sub-market and market basis, to facilitate understanding of where in the cycle the market sits at any particular moment.

Ends